5 September, 2023

What is hydrocarbon accounting?

Description

Hydrocarbon accounting (HCA), is defined as “the system by which ownership of oil, gas, gas liquids and produced water is determined and tracked from the point of production to a point of sale or discharge”. The terms allocation and production reporting are also commonly used to refer to this function.

It has two essential elements. Firstly, gathering and validating flow measurement data in order to establish the definitive record of production from a facility. Secondly, it involves carrying out allocation calculations on the flow measurements to derive quantities that are not measured directly.

Why is it important?

Throughout the world it is a legislative requirement to report production quantities to government. These reports are generated by the HCA process.

In the case of a joint venture or third-party infrastructure sharing arrangement, HCA determines the ownership of commingled flows. It therefore affects the revenue each partner receives.

Finally, hydrocarbon accounting provides important information to administrators, managers and engineers throughout the organisation.

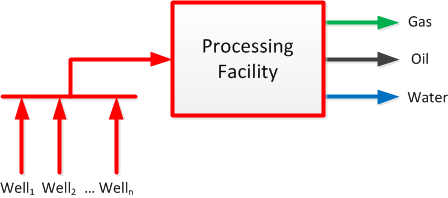

Allocation procedures vary in complexity from the trivial to the highly complicated. A simple but very common requirement is to allocate the metered gas, oil and water streams leaving a facility to the wells from which the fluids were produced, as shown in figure 1.

Figure 1

Here, the metered flows are simply divided between the wells in proportion to the best estimate of each well’s production of each phase. The estimate may come from the latest well test, a multi-phase meter or a well model.

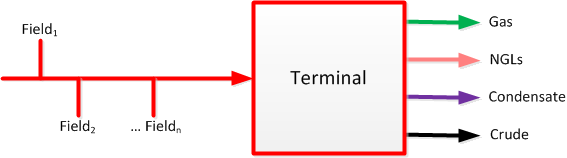

At the other end of the complexity scale is the requirement to allocate the products leaving a large processing plant or terminal between the fields and field owners whose production was delivered to the facility, as in figure 2. As well as the quantities delivered by each field, the calculation also needs to take account of the different qualities of the fields’ fluids, the plant conditions and many other factors. In many cases, an acceptable level of accuracy can only be achieved with the use of a process model to simulate the behaviour of each field’s molecules as they pass through the plant.

Figure 2

What is required to manage Hydrocarbon Accounting successfully?

An effective HCA function must include the following:

- A well-defined allocation procedure, in which the input data and calculations are specified in detail, and which is approved by all relevant parties.

- A computer system which can collect and store the data, perform the calculations and generate the required reports. The system must apply a high degree of control over access to data and calculations in a multi-user environment. Spreadsheets are widely used, but while they are capable of carrying out allocation calculations, they lack these controls.

- Clear definition of roles and responsibilities.

What goes wrong?

Hydrocarbon accounting can be a complicated business, so much so that the accurate and reliable collection, calculation and presentation of data often present a challenge. When it comes to errors, the following themes recur consistently.

- Failure to establish one version of the truth. There must be a single database that is accepted as the definitive source of production data, accessible to everyone in the organisation who needs it. Without this, errors abound and time is wasted on reconciling conflicting numbers.

- Insufficient control over corrections. An important function of an Hydrocarbon Accounting system is to allow corrections to measurement data. However, if this is not accompanied by a high degree of control then inconsistencies inevitably occur and can be very difficult to resolve.

- Checking for consistency rather than accuracy. The diligent hydrocarbon accountant will always check his or her results before distributing them. However, such checks often only ensure that the data all adds up correctly, without applying independent tests of accuracy. This can lead to serious errors going undetected for long periods, caused by such issues as out-dated sample data or equations used outside their valid ranges.

- Allowing uncontrolled changes to allocation calculations. Confidence in HCA results depends on a well understood and accepted set of calculations being carried out reliably. Nothing erodes confidence more quickly than unexplained errors appearing in the calculations. This is especially prone to happen with spreadsheets that do not separate calculations from data.

For owners and operators of oil and gas fields, HCA plays a key role in determining their revenues; it is the cash register of the business. Therefore it deserves careful attention.

This article is also featured in Energy Update magazine.

Search

Other Resources

Uncertainty based allocation

Emissions Reporting in Axis

Production losses

Services